What are the markets really telling you? — Week of January 16, 2023

Essential Economics

— Mark Frears

Connecting?

How many Allen wrenches do you have around the house? Are they the single ones left over from an Ikea construction, or a nice set of multiple sizes? The bolt that the Allen wrench fits was designed for safety, as it is flush with the surface. It can’t catch on clothing as was happening in factory accidents before this concept was patented in 1909. The hex wrench fits very well into the humble bolt, if you have the right size for the job. The markets do not have as good a connection in some areas.

Short-term rates

Due to inflation’s impact on prices and the current laser-focus of the Fed, we are paying particular attention to the Fed Fund’s (FF) target rate. This is the rate the Federal Open Market Committee (FOMC) changes to indicate their intention on tightening or loosening financial conditions. They are currently tightening financial conditions by raising short-term rates as this will cause other rates to increase, making things more expensive. The desired outcome is for demand to slow. If demand slows, the economy slows and prices will not be able to stay elevated, causing suppliers of goods and services to lower prices, and inflation to abate.

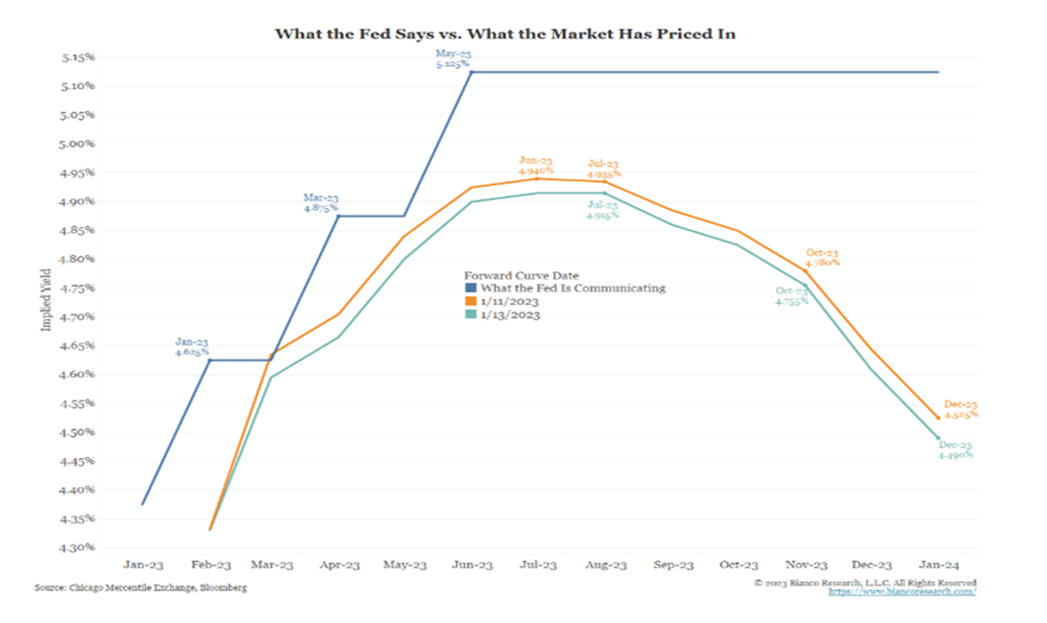

The Fed communicates their guidance for future FF rate moves through the quarterly “dot plot” as well as speeches given by members of the FOMC. The market communicates its expectations through the FF futures. As you can see below, the dark blue line is what the Fed is telling us. They expect to raise this rate to close to 5.15% and leave it steady there for the rest of this year. The futures markets are not on the same page! Indicated by the other two lines below, they expect the inflation picture will improve enough and for there to be recession fears later this year, causing the Fed to start lowering this rate.

Who will be right? You may have heard the expression, “don’t fight the Fed,” as they are going to be right, but markets are disconnected currently.

Goods and services

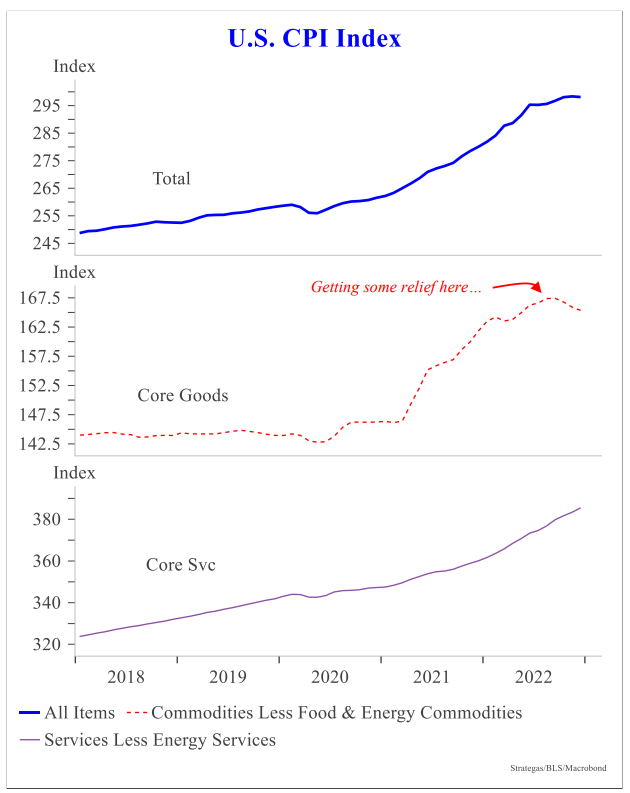

A disconnect associated with inflation is the costs associated with goods versus services. Much of what drove goods inflation had to do with supply chain disruption and that is no longer a factor in most cases. Therefore, as you can see below, the portion of inflation associated with goods’ prices is decelerating. This is what is driving the improvement in the overall Consumer Price Index (CPI) metric.

On the other hand, services inflation continues an upward trajectory. This is primarily driven by labor costs, and we have seen the disconnect between supply and demand in the labor market. Therefore, this lends credence to the case for the Fed versus the markets.

Source: Strategas Research

While we are seeing improvement in inflation numbers on a year-over-year basis, we still must keep in mind that prices are at elevated levels compared to long-term trends and Fed targets.

Real rates

A very common disconnect happens when “rates” are discussed. First, what term, or maturity, of rate are you referring to, and second, are you considering inflation in your view?

The yield curve, as displayed below, indicates rates from a one-month term all the way out to a thirty-year term. So, when you say, “rates are rising,” you must be more specific. The overnight FF target rate the Fed controls directly influences the short-term part of this curve but can indirectly guide the long end as well. The Fed’s movement of short-term rates conveys a message to the longer end, about future rate moves. Longer-term rates are driven by inflation expectations and economic growth expectations. For instance, if you lend money for five years, how much interest should be charged? More moving parts, the further out the curve you go.

Source: Bloomberg

The second disconnect concerns the impact of inflation. The rates we are looking at above are nominal interest rates, as inflation is part of these rates. Real rates are nominal rates less inflation.

Real rates give you a better view of what is really happening. For instance, let’s say you got a 3% raise in salary, and you are feeling pretty good about that. If inflation is running at the Fed’s long-term target of 2%, you had a “real” increase of 1%. Not great, but at least it is positive. With inflation currently running at 6.5%, your real increase was a negative 3.5%. While you are earning more, inflation is taking a bigger bite out of your purchasing power.

Therefore, dig deeper when people start talking about interest rates and find out if they understand what they are really dealing with.

What to watch

The many disconnects in the markets can provide opportunity for arbitrage, if everyone is not on the same page. Pay attention to what the market is telling you with real numbers instead of only reading the headlines.

Wrap-up

It is very important to have solid connections in all areas of your life, and if some are disconnected, it helps to dig deeper and understand the implications.

| Upcoming Economic Releases: | Period | Expected | Previous | |

|---|---|---|---|---|

| 17-Jan | Empire Manufacturing | Jan | (8.6) | (11.2) |

| 18-Jan | NY Fed Services Business Activity | Jan | N/A | (17.6) |

| 18-Jan | Retail Sales MoM | Dec | -0.9% | -0.6% |

| 18-Jan | Retail Sales ex Autos MoM | Dec | -0.5% | -0.2% |

| 18-Jan | Producer Price Index MoM | Dec | -0.1% | 0.3% |

| 18-Jan | PPI ex Food & Energy MoM | Dec | -0.1% | 0.4% |

| 18-Jan | Producer Price Index YoY | Dec | 6.8% | 7.4% |

| 18-Jan | PPI ex Food & Energy YoY | Dec | 5.5% | 6.2% |

| 18-Jan | Industrial Production MoM | Dec | -0.1% | -0.2% |

| 18-Jan | Capacity Utilization | Dec | 79.6% | 79.7% |

| 18-Jan | Business Inventories | Nov | 0.4% | 0.3% |

| 18-Jan | NAHB Housing Market Index | Jan | 31 | 31 |

| 18-Jan | Federal Reserve releases Beige Book for Jan 31-Feb 1 FOMC meeting | |||

| 19-Jan | Building Permits | Dec | 1,370,000 | 1,342,000 |

| 19-Jan | Building Permits MoM | Dec | 1.4% | -11.2% |

| 19-Jan | Housing Starts | Dec | 1,357,000 | 1,427,000 |

| 19-Jan | Housing Starts MoM | Dec | -4.9% | -0.5% |

| 19-Jan | Philadelphia Fed Business Outlook | Jan | (11.0) | (13.8) |

| 19-Jan | Initial Jobless Claims | 14-Jan | 214,000 | 205,000 |

| 19-Jan | Continuing Claims | 7-Jan | 1,655,000 | 1,634,000 |

| 20-Jan | Existing Home Sales | Dec | 3,950,000 | 4,090,000 |

| 20-Jan | Existing Home Sales MoM | Dec | -3.4% | -7.7% |

Mark Frears is an Investment Advisor, Executive Vice President, at Texas Capital Bank Private Wealth Advisors. He holds a Bachelor of Science from The University of Washington, and an MBA from University of Texas – Dallas.

The contents of this article are subject to the terms and conditions available here.