Summer’s over – and so is the rally – Week of September 6, 2022

Strategy and Positioning written by Steve Orr, Chief Investment Officer; and Essential Economics written by Mark Frears, Investment Advisor

| index | wtd | ytd | 1-year | 3-year | 5-year | index level |

|---|---|---|---|---|---|---|

| S&P 500 Index | -3.23 | -16.78 | -12.21 | 12.35 | 11.58 | 3,924.26 |

| Dow Jones Industrial Average | -2.85 | -12.54 | -9.85 | 8.50 | 9.69 | 31,318.44 |

| Russell 2000 Small Cap | -4.70 | -18.72 | -20.51 | 8.43 | 6.39 | 1,809.75 |

| NASDAQ Composite | -4.18 | -25.24 | -23.55 | 14.87 | 13.63 | 11,630.86 |

| MSCI Europe, Australasia & Far East | -4.76 | -21.31 | -22.43 | 2.13 | 1.58 | 1,790.17 |

| MSCI Emerging Markets | -3.00 | -18.79 | -23.12 | 2.83 | 0.49 | 976.14 |

| Barclays U.S. Aggregate Bond Index | -1.40 | -11.28 | -12.13 | -2.25 | 0.43 | 2,089.40 |

| Merrill Lynch Intermediate Municipal | -0.60 | -7.47 | -7.66 | -0.71 | 1.16 | 296.19 |

As of market close September 2, 2022. Returns in percent.

Strategy & Positioning

— Steve Orr

Summer's over

Although the 1st marks the traditional end of summer, for the Bulls summer ended on August 18. Since mid-August, U.S. stock indices have given up roughly half of the summer rally’s gains. Bonds had it worst, with high quality names giving up all of their price gains. What ruined the rally? There is always more than one bad actor in Bear cycles, but we’ll start with the Fed.

Over the last year, markets did not take the Fed seriously. For sure the Fed was too late in starting to raise interest rates. The Fed has staunchly sought 2% inflation over the last two decades. So, you can imagine we were quite perplexed when consumer price inflation hit 7.9% in February of this year before the Fed even began to raise rates. That was too late even for Fed standards. Recall that in February a year earlier CPI was 1.7%. Hey that’s close enough for 2% and horseshoes, Fed. Call it victory and go back to managing the money supply. April 2021’s reading of 4.2% should have spurred the FOMC to action but it did nothing.

Wall fight

Wall Street consistently projects inflation rolling over and heading toward 2% in the next couple of years. Essentially economists are trying to validate the Fed’s long-sought goal: return inflation to a “magical” 2% level. Current futures pricing for Fed Funds projects the Fed will stop raising rates next spring. The opinion expressed by pit traders is that the peak rate will average around 3.85%. Well, that is close to 4%, but still below. What are FOMC members saying? Above 4% short rates and keep them above that level for “some time.” What does Wall Street know that the Fed does not?

The Fed believes the only way to curb inflation is to kill demand. Aggregate demand comes from consumer spending and industrial new orders. Forcing interest rates high enough and withdrawing liquidity to the point where businesses stop expanding and start laying off workers is the tactic. Raising unemployment from 3.7% to at least 4.5% is their objective. Putting people out of work will, in theory, curb consumer spending. New orders and production surveys show that manufacturing is already meaningfully slowing.

Looking ahead, fuel and fertilizer appear to be in tight supply. These inputs will pressure global food prices higher over the next couple of years. Computer chips are said to have rolling supply shortages as plants re-tool for new models and assemblers restart and shut. Wall Street may cheer lower inflation in the coming months. Remember CPI figures are the rate of change of prices. When CPI “drops” it just means prices are not rising as quickly as they were earlier. Prices are still going up. And no, we are not going back to 2019 prices on anything, anytime soon. A good portion of commodity and hard goods inflation comes from supply problems. Consumer inflation in this cycle has been driven by fiscal policy: spending by the government. The Fed is trying to curb both by focusing on employment. As with the shutdowns, we are in a global economic experiment. In uncharted waters, stick with the great Marty Zweig and Ned Davis: “Don’t Fight the Fed.”

Lower all over

The headline payrolls number would make one think the economy is fine. Indeed, it’s not in bad shape at all. Fast money trades on how fast the change is changing (the second derivative if you care). In 2021 we were all about 2022 sliding gently lower toward trend growth. The economy’s rate of change would slow but still result in positive growth.

The ride has been bumpier and to lower levels than our base case. We may look back on 2022 and 2023 as a time of rolling recessions, where the big picture numbers, like payrolls and job openings, are fine, but pockets of the economy take their turn in no or negative growth mode.

One thing the Street should know is that the economic data is worse than at the lows of June 16. Factory orders, production and retail spending are at best flat over the last three months. Adjusting for inflation, retail sales year-over-year are down 4%. Wages are growing, but slower than inflation. If production and spending are not keeping up, then company profit margins will not. Walmart was the canary in the earnings coal mine. We think. We may be early, but we believe third quarter earnings are going to feature managements lowering earnings expectations for this year and next.

Cloudy outlook

On the 21st of September there was never a cloudy day (Earth, Wind, & Fire reference). On the 21st of this month the Fed should raise rates again. What would part investors’ clouds? One ray of sunshine would be an admission that, yes, we the Fed are behind, but we will not “rush and squash” the economy just to choke off demand. Another admission would be that the Fed will continue its increases but in a steady, every-meeting tempo.

September is historically a bumpy month for investors. Since World War II it holds the bottom spot in terms of return performance for stocks. September tends to be a trend reinforcer. Our trusty Stock Trader’s Almanac tells us that if stocks are in a downtrend coming into the month, returns average -2%. If they are in an uptrend, the S&P 500 posts an average loss of 0.5%.

There is always the question, “if it’s going down, then why not get out?” That is a trading tactic that, for pros, has a less than satisfactory track record. For intermediate and longer time horizons it can do lasting damage. We have watched this “going down, get out” tactic, and time and again, gains are forever lost after the exit. This cycle appears to be a non-recession Bear, a pause in a long-term Secular Bull. If a recession follows, the Bear may stick around a few months longer. The one Bull marker we have on our board is the mid-term election cycle. Averaging all mid-term years back to the 1920s shows a rally starting around Halloween. We would welcome a treat or two.

Wrap-up

August’s 4% slide from the summer rally marked a return to the Bear cycle. Ned Davis calculates that since 1900, Cyclical (short-term) Bears with no recession inside of a Secular Bull average about a 23% drop and last just under 200 trading days. If this is an average Bear (no Yogi jokes) then Halloween is about right for a mid-term election rally.

Essential Economics

— Mark Frears

A calling, or a way to pay the bills?!

My first job was throwing papers after school, and I saved enough money to buy a canoe that is still at our family cottage. I worked my way through college as a lifeguard and had summer jobs as well. Post-college I worked in a salmon cannery, on a Japanese trawler and helped design an aquarium exhibit. Eventually I started as an assistant on the trading floor of a bank, and the rest is history. Bottom line, I have been employed and supporting myself since college. What is different now?

Payroll release

The latest “big” and highly anticipated economic release was the August Non-farm Payroll numbers. On the surface, the 315,000 jobs gained last month were in line with expectations, and not showing a slowing job market. The markets chose to dig a bit deeper to better understand. First, there was a downward revision of 107,000 jobs to the last two month’s results. This tells us a job markets were not as strong as initially portrayed. Second, the unemployment rate rose 0.2% to 3.7%. The fact that there were more people looking for jobs could indicate the labor market is not as strong as in recent months.

Look at this in the context of the current environment. Bad news, slowing labor market, is perceived as good news as this means the Fed will not have to raise rates as much to slow the economy. Clear as mud? With inflation still stubbornly high, the Fed will use their primary tool of increasing short-term rates until inflation is back closer to their long-term target of 2%. Therefore, if the labor market shows signs of weakness, we decrease the risk of a severe recession associated with job losses, as the Fed would not have to push us to that extreme.

Demographics

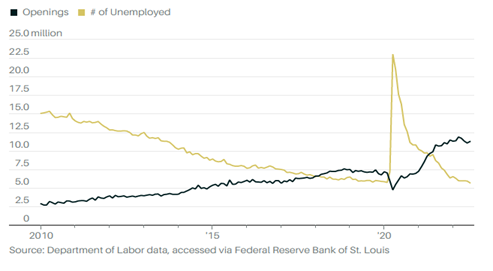

Why are there more job openings than available workers?! We continue to see the Job Openings and Labor Turnover Survey (JOLTS) show over 11 million openings for workers, yet our unemployment rate is close to historic lows at 3.7%.

The total number of people working is now 240,000 above February of 2020 when the pandemic began. The most likely conclusion for this disparity would be that our population of workers has shrunk. Who has left?

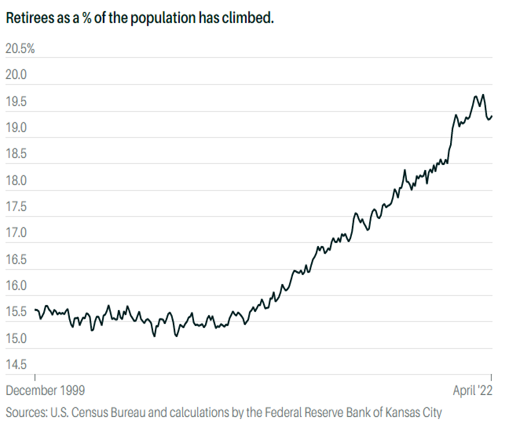

First, let us talk about the Baby Boomers. We knew this was going to happen, and the pandemic effect accelerated this. The chart below shows the steady 15.5% of the population has accelerated up to 19.5%. That is significant. One of the unknowns is whether they will get bored or feel a financial pinch and come back to work. I think some will.

Second, pandemic effects have kept people from coming back to work. Some of this is related to long-term Covid where health does not recover fully, and some is due to personal decisions. The personal choices may relate to working from home, work-home balance or family obligations. It is very hard to quantify this impact and whether it will be sustained or revert to normal trends. The work from home trend will have an impact on working spaces (commercial real estate) as well.

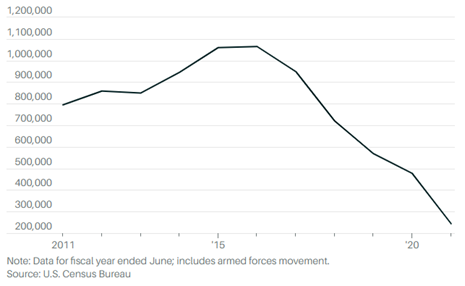

Third, legal immigration has slowed materially, removing workers from highly educated scientists and engineers to manual laborers. Three fields impacted are healthcare, construction and STEM (science, technology, engineering and math) professions. Traditionally these fields have grown their workforces through immigration, and that decline can be seen below.

All these factors can have long-term effects, making the Fed’s job of slowing the job market, and mitigating the rising cost of hiring workers more difficult.

Fed

Like the stock and bond markets, we come back to the Fed and the Federal Open Market Committee (FOMC). While last week’s Non-farm Payroll number may have given some short-term solace on the worrisome job front, they have reiterated that they still have work to do.

Their inflation target is 2% for the Personal Consumption Expenditures (PCE) measure and it is more than double that currently. The lack of available workers will continue to push wages and compensation up, causing them to have to raise short-term rates more than they would like to slow the economy and hit their inflation target. They have said they will put people out of work to achieve this goal.

The next regular FOMC meeting is September 20 – 21 and short-term futures are split between a 50- or 75-basis point increase. The terminal/high rate is 3.85% in March 2023, per Fed Funds futures.

Wrap-up

There has also been talk of lower drive or desire to work in the current environment. That is very difficult to quantify/verify. I know that the variety of jobs that I have experienced has exposed me to new things to learn and great people to work with at every stop. I would not change that for anything.

| Upcoming Economic Releases: | Period | Expected | Previous | |

|---|---|---|---|---|

| 6- Sep | S&P Global US Services PMI | Aug | 44.2 | 44.1 |

| 6- Sep | S&P Global US Composite PMI | Aug | 45.0 | 45.0 |

| 6- Sep | ISM Services Index | Aug | 55.4 | 56.7 |

| 7- Sep | MBA Mortgage Applications | 2-Sep | N/A | -3.7% |

| 7- Sep | Trade Balance | Jul | -$70.3B | -$79.6B |

| 7- Sep | US Federal Reserve release Beige Book for Sep 20-21, 2022 Meeting | |||

| 8-Sep | Initial Jobless Claims | 3-Sep | 240,000 | 232,000 |

| 8-Sep | Continuing Claims | 27-Aug | 1,438,000 | 1,438,000 |

| 8-Sep | Consumer Credit | Jul | $33.000B | $40.154B |

| 9-Sep | Wholesale Trade Sales MoM | Jul | 0.8% | 1.8% |

| 9-Sep | Wholesale Inventories MoM | Jul | 0.8% | 0.8% |

| 9-Sep | Household Change in Net Worth | Q2 | n/a | -$544B |

Steve Orr is the Executive Vice President and Chief Investment Officer for Texas Capital Bank Private Wealth Advisors. Steve has earned the right to use the Chartered Financial Analyst and Chartered Market Technician designations. He holds a Bachelor of Arts in Economics from The University of Texas at Austin, a Master of Business Administration in Finance from Texas State University, and a Juris Doctor in Securities from St. Mary’s University School of Law. Follow him on Twitter here.

Mark Frears is an Investment Advisor at Texas Capital Bank Private Wealth Advisors. He holds a Bachelor of Science from The University of Washington, and an MBA from University of Texas – Dallas.

The contents of this article are subject to the terms and conditions available here.