Housing — Week of March 6, 2023

Essential Economics

— Mark Frears

A place to lay your head

On February 22, 1980, I was driving a van across Montana, listening to the radio for the outcome of the U.S. versus Russia hockey game. The Miracle happened and the van celebrated. Looking out the windows at the surrounding area, there were very few houses. At that time, the Consumer Price Index (CPI) was 14.2% on a year-over-year basis and Fed Funds were at 15%! Now, while inflation is elevated, we are at only half of that level, and Fed Funds have not caught up with CPI yet. Houses are still hard to find.

Rates

One thing we know for certain is that rates are higher now than they were a year ago. The 10-year U.S. Treasury (UST) note, shown below, has risen from 1.50% to 4%. This is a 167% increase, over a relatively short period.

Source: Bloomberg

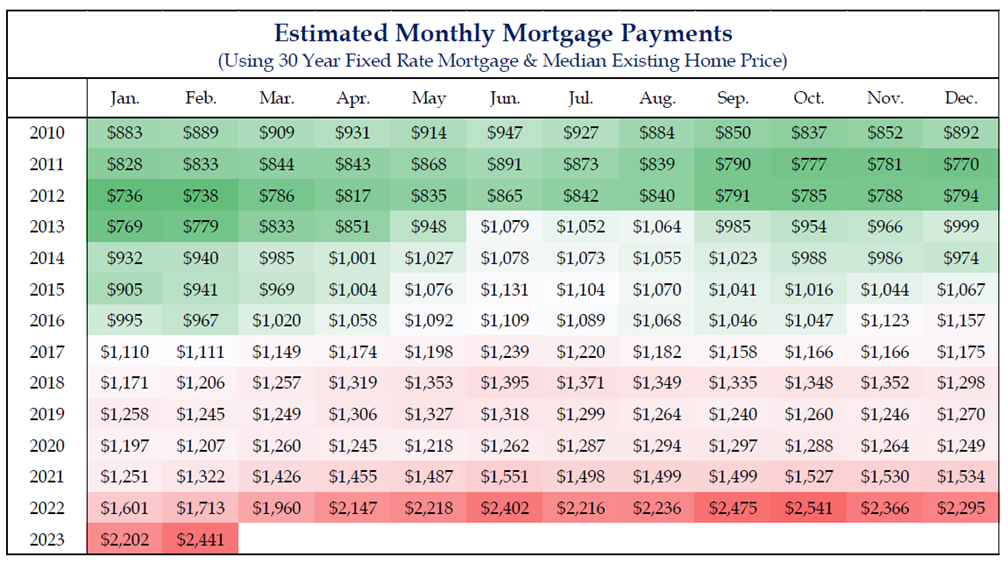

This increase reflects the inflationary economic environment we are currently in. The recent rise is an acknowledgment that we are not yet done with higher prices. The 10-year UST is a good proxy for mortgage rates, and this increase has been felt by new home buyers, as you can see below.

Source: Strategas

Given a 30-year mortgage and median existing home price, your new purchase mortgage payment would have doubled compared to January 2021. If you locked in your mortgage payment prior to the run-up in rates, you are looking good.

Housing

As the housing market is highly dependent on direction of interest rates, it is a leading indicator as to the health of the economy.

One of the first things to watch is applications for building permits, as a sign of future activity. As you can see below, since the recent peak at the end of 2021, this has been on a downward slide.

Source: Bloomberg

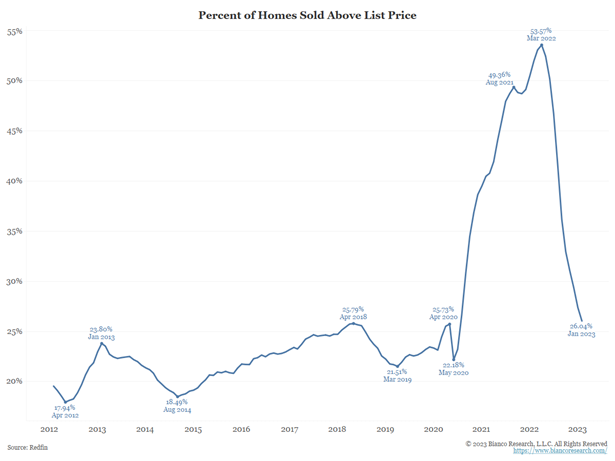

Home prices are another indicator of activity in this sector. While we were seeing homes sell for over asking price on a regular basis in desirable areas, this is no longer the case. As you can see below, we are back down to more historical averages with 26% of homes selling above list price.

Source: Bianco Research

We have established that the housing market has slowed materially. What impact does this have on the economy?

According to the National Association of Home Builders (NAHB), housing contributes 15-18% of Gross Domestic Product (GDP). Residential investment makes up 3-5% and is primarily related to construction of single family and multifamily structures. This also captures remodeling, which usually increases when people must stay in homes longer than they expected. Consumption spending makes up 12-13% of GDP is housing services like rent, mortgage and utility payments. This is a significant portion of the economy.

Looking ahead

Recession coming? Housing is a leading indicator and one of the first sectors to respond to interest rates. Both of those characteristics make it worth watching. The focus right now is on the Fed and labor markets, which is justified, but remember that labor is at best a coincident, and more likely a lagging indicator.

One other concern for the post-recession environment is that with supply of housing not increasing, when demand comes back with a vengeance, home prices will remain high. We need a time of adding to supply without increased demand to bring these back down. We’ll see if we get that.

Wrap-up

While the “Miracle on Ice” was one of the sports highlights of my time, the economic times back then were not great. The hope and uplift the win created were much needed. We are once again living in uncertain times, and it makes good sense to pay attention to leading indicators like the housing market.

| Upcoming Economic Releases: | Period | Expected | Previous | |

|---|---|---|---|---|

| 6-Mar | Factory Orders | Jan | -1.8% | 1.8% |

| 7-Mar | Wholesale Inventories MoM | Jan | -0.4% | -0.4% |

| 7-Mar | Consumer Credit | Jan | $25.000B | $11.565B |

| 8-Mar | ADP Employment Change | Feb | 200,000 | 106,000 |

| 8-Mar | JOLTS Job Openings | Jan | 10,584,000 | 11,012,000 |

| 9-Mar | Challenger Job Cuts YoY | 4-Mar | N/A | 440.0% |

| 9-Mar | Initial Jobless Claims | 4-Mar | 195,000 | 190,000 |

| 9-Mar | Continuing Claims | 25-Feb | 1,659,000 | 1,655,000 |

| 10-Mar | Change in Nonfarm Payrolls | Feb | 215,000 | 517,000 |

| 10-Mar | Change in Private Payrolls | Feb | 215,000 | 443,000 |

| 10-Mar | Unemployment Rate | Feb | 3.4% | 3.4% |

| 10-Mar | Average Hourly Earnings MoM | Feb | 0.3% | 0.3% |

| 10-Mar | Average Hourly Earnings YoY | Feb | 4.7% | 4.4% |

| 10-Mar | Labor Force Participation Rate | Feb | 62.4% | 62.4% |

| 10-Mar | Underemployment Rate | Feb | N/A | 6.6% |

Mark Frears is an Investment Advisor, Executive Vice President, at Texas Capital Bank Private Wealth Advisors. He holds a Bachelor of Science from The University of Washington, and an MBA from University of Texas – Dallas.

The contents of this article are subject to the terms and conditions available here.