Extremes — Week of March 27, 2023

Essential Economics

— Mark Frears

Down and up

When I was on a Japanese fishing trawler in the Bering Sea, north of the Aleutian Islands, we saw some severe weather. One day we had nine-meter seas. What does that mean? The distance between trough and peak of the waves was over 27 feet! Those were some extremes I did not want to see very often. The market is seeing some extreme changes lately; what will you do in response?

Interest rates

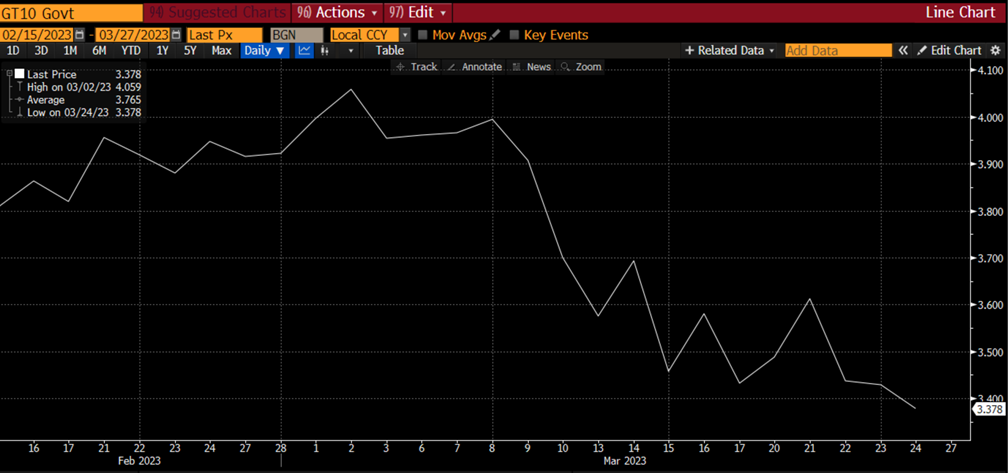

There have been a few changes in interest rates over the last couple of weeks. When the news started to surface of a large, failing financial institution hit the wires, markets reacted. The percolating idea of an upcoming recession became much more real. As the chart below shows, U.S. Treasury (UST) 10-year note dropped from 3.99% to 3.46% in a matter of days. That is material shift.

Sources: Bloomberg

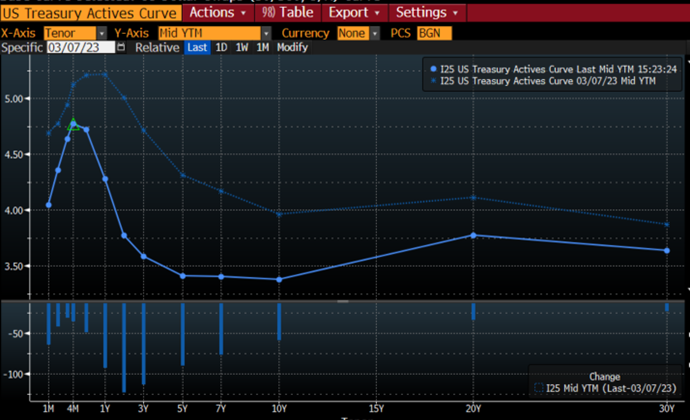

Not only the 10-year moved, but the entire curve shifted as you can see below. This shows the shift from March 7 until March 23. Most parts of the curve moved down 50 basis points (bp), but some areas over 100bp. This will make mortgages cheaper and corporate borrowings less expensive. A good consequence.

Sources: Bloomberg

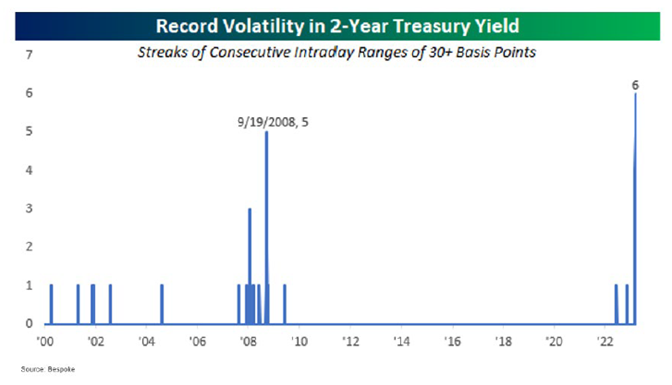

Not only were the day-to-day changes huge, but the intra-day swings were larger than 2008. As you can see below, the two-year UST has had six consecutive days of swings over 30bp. Whoa.

Sources: Bespoke

While the markets were aware of a material shift in expectations, it was not a one-and-done shift, but an extremely volatile move lower. There was uncertainty along with the impact.

Equities

What was going on in the equity market when the bond market decided to price in some sort of coming recession? The initial focus was on financial institutions, as Silicon Valley and Signature failed over the weekend of March 10. First Republic is an example of an “at risk” bank — still afloat, but with some help. You can see the slide in the stock price from around $120 per share, down to just over $12 per share. If you owned 1,000 shares, you just lost $108,000 in market value.

Sources: Bloomberg

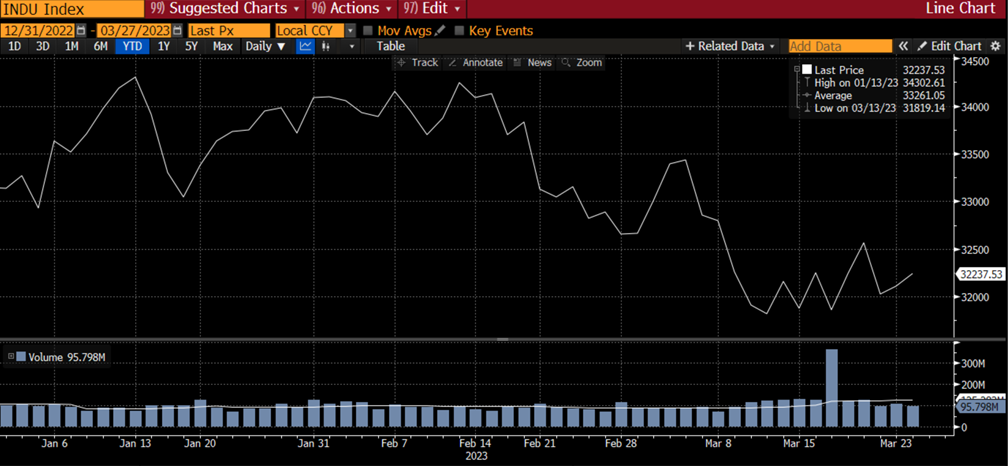

While the Dow Jones Industrial Average did make a material drop as the news in the financial sector came out, we have seen some effort at recovery from that slide.

Sources: Bloomberg

One of the takeaways here is that this is not a systematic event as we saw in 2007-2008. What came to light was this was a few banks that were not managed properly, given the risk they had on their balance sheets. As we have been talking about the upcoming recession for some time, this mismanagement brought further attention to that possibility.

Federal Open Market Committee (FOMC)

Last week was the FOMC’s scheduled meeting. They were in the hotseat even more, given the stress showing up in financial markets. Futures markets had dropped expectations of a possible 50bp hike, down to a toss-up between no move and a 25bp hike. The market was coming in line with where the Dot Plot showed the peak Fed Funds rate, at 5.10%, but now the futures market expects cuts in rate sooner as recession will be here soon.

Recall the Fed’s two-pronged goal of full employment and stable prices. Did the failure of two U.S. banks suddenly fix the inflation issue we have with the Consumer Price Index at 6%?! I don’t think so. The Fed had to continue to raise rates to fight the inflation battle, while acknowledging the more fragile financial sector. They did that with a 25bp hike and changes in verbiage in the press release.

The Fed did acknowledge that banks may be less reluctant to lend, given the current fear of bank deposit runs and additional scrutiny, but this may assist them in slowing the economy. They also stated their continued focus on current data to drive their future moves. The next meeting is not until May 3, and futures currently have a pause in rate moves priced in.

Big picture

As we know, you and I are two-thirds of economic growth. Considering the recession talk over the last six months, have you changed your spending habits or behavior? Will this last couple of weeks impact your behavior? I believe it might start to make you think a bit more. Even if this has not impacted you directly, you know someone who has had to change their spending habits.

If you start to reconsider major purchases, push out vacations or change your daily spending habits, we will see a slowdown in the economy. Perhaps this was a wakeup call or needed market adjustment. These types of market movements also create opportunities. Where do you see something that is overdone? The Fed would like to see a slowdown and not a full stop on the economy. That would help bring inflation back down, which will help us all.

Economic releases

The markets paid little attention to economic news last week. We had stronger than expected housing sales, continued tight labor markets indicated by low Jobless Claims, and declines in Durable Goods orders. Nothing extreme, but continuing not too hot, not too cold.

This week, we have the Conference Board’s Consumer Confidence, Personal Income and Spending, Personal Consumption Expenditures (Fed favorite inflation measure) and the UM Consumer Confidence. Unless these come in extremely different than expectations, the markets will stay focused on the Fed, financial institutions and interest rates.

Wrap-up

Extreme times can call for you to act. On the Japanese trawler, I wedged the life vest under the outside edge of my mattress to make sure I did not roll out at night. In the current market, you should be aware of the signals the market is sending, alerting you to more volatility ahead.

| Upcoming Economic Releases: | Period | Expected | Previous | |

|---|---|---|---|---|

| 27-Mar | Dallas Fed Manufacturing Activity | Mar | (10.0) | (13.5) |

| 28-Mar | Wholesale Inventories MoM | Feb | -0.1% | -0.4% |

| 28-Mar | Retail Inventories MoM | Feb | 0.2% | 0.3% |

| 28-Mar | FHFA House Price Index MoM | Jan | -0.3% | -0.1% |

| 28-Mar | S&P CoreLogic Home Price 20-City YoY | Jan | 2.50% | 4.65% |

| 28-Mar | Conf Board Consumer Confidence | Mar | 101.0 | 102.9 |

| 28-Mar | Conf Board Present Situation | Mar | N/A | 152.8 |

| 28-Mar | Conf Board Expectations | Mar | N/A | 69.7 |

| 28-Mar | Richmond Fed Manuf Index | Mar | (9) | (16) |

| 28-Mar | Richmond Fed Business Conditions | Mar | N/A | (6) |

| 28-Mar | Dallas Fed Services Activity | Mar | N/A | (9.3) |

| 29-Mar | Pending Home Sales MoM | Feb | -3.0% | 8.1% |

| 30-Mar | Initial Jobless Claims | 25-Mar | 196,000 | 191,000 |

| 30-Mar | Continuing Claims | 18-Mar | 1,697,000 | 1,694,000 |

| 30-Mar | GDP Annualized QoQ | Q4 | 2.7% | 2.7% |

| 30-Mar | Personal Consumption | Q4 | 1.4% | 1.4% |

| 31-Mar | Personal Income | Feb | 0.2% | 0.6% |

| 31-Mar | Personal Spending | Feb | 0.3% | 1.8% |

| 31-Mar | Real Personal Spending | Feb | -0.2% | 1.1% |

| 31-Mar | PCE Deflator YoY | Feb | 5.1% | 5.4% |

| 31-Mar | PCE Core Deflator YoY | Feb | 4.7% | 4.7% |

| 31-Mar | MNI Chicago PMI | Mar | 43.0 | 43.6 |

| 31-Mar | UM (Go MSU) Consumer Sentiment | Mar | 63.4 | 63.4 |

| 31-Mar | UM (Go MSU) Current Expectations | Mar | N/A | 66.4 |

| 31-Mar | UM (Go MSU) Expectations | Mar | N/A | 61.5 |

| 31-Mar | UM (Go MSU) 1-yr inflation | Mar | 3.8% | 3.8% |

| 31-Mar | UM (Go MSU) 5- to 10-yr inflation | Mar | 2.8% | 2.8% |

Mark Frears is an Investment Advisor, Executive Vice President, at Texas Capital Bank Private Wealth Advisors. He holds a Bachelor of Science from The University of Washington, and an MBA from University of Texas – Dallas.

The contents of this article are subject to the terms and conditions available here.