Economic battle — Week of February 27, 2023

Essential Economics

— Mark Frears

Opposing forces

Growing up, my brother and I fought all the time. He was the popular athlete, and I was the bookworm. We ran in different circles and when we were at home, there was not much common ground. Fortunately, time goes by, and we are very close now, so there is always hope! There are two significant forces at play in the economy right now, each with their own separate agendas. There will be an ongoing confrontation until we reach conclusion.

The Fed

Force number one is the Federal Reserve Bank, on their mission to fight price inflation. Their primary tool in this battle is the overnight Fed Funds (FF) rate. This short-term rate doesn’t necessarily influence the longer end of the yield curve, but it is how they communicate their intentions.

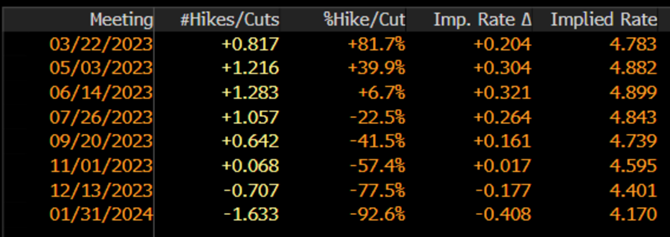

At the February 1 meeting, they raised the FF rate by 0.25% to a range of 4.50 to 4.75%. This 25-basis-point (bp) move was the smallest rate move in the hiking cycle and possibly sent the message that they were pausing to allow previous moves to work their way through the system, or close to the top. The FF futures at that time reflected expectations that the peak rate would be 4.899% in June, as you can see below.

Source: Bloomberg

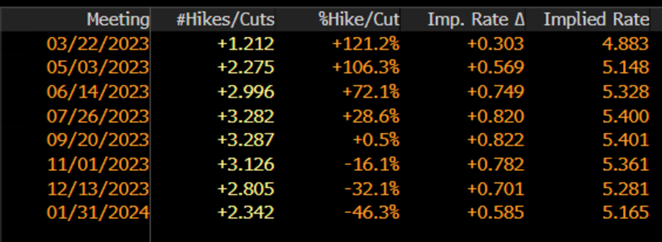

Fast forward three weeks and the world has changed. Futures now reflect a peak rate of 5.401% in September.

Source: Bloomberg

We are looking at a change of 50bp in three weeks and staying higher for longer. If you compare the December meetings above, current expectations for year-end are 0.88% higher than on February 2.

What has changed? First, while Consumer Price Index and Producer Price Index continued lower on a year-over-year basis, there are starting to be some categories where this trend is slowing. Services are the prime focus here. Second, the labor market continues to show strength. The non-farm payroll for January was supposed to show an addition of less than 200,000. The actual number of new workers was 517,000! If employers continue to hire at this pace, in the face of fewer workers available, wage inflation will be a concern. Third, the Fed Governors and Presidents have been out in force saying, “higher for longer.” There is an expression, “don’t fight the Fed” and the markets are starting to pay a bit more attention.

The consumer

Enter force number two, you and I. Two-thirds of the economy is driven by the consumer, reflected in the Gross Domestic Product (GDP).

Last week, Personal Spending for January showed a strong uptick as you can see below. Consumers are not changing their behavior, despite the Fed’s attempts to slow them down.

Source: Bloomberg

This highlights one of the weaknesses of the Fed on the economic battlefield. They are raising rates, trying to slow economic supply by making it more expensive to borrow, and causing companies to slow production. The issue here is that they have no impact on demand, and the consumer continues to spend.

In a slowing economy, you would expect to see more people out of work, yet the jobless claims filed by people out of work are still at historically low levels, as you can see below.

Source: Bloomberg

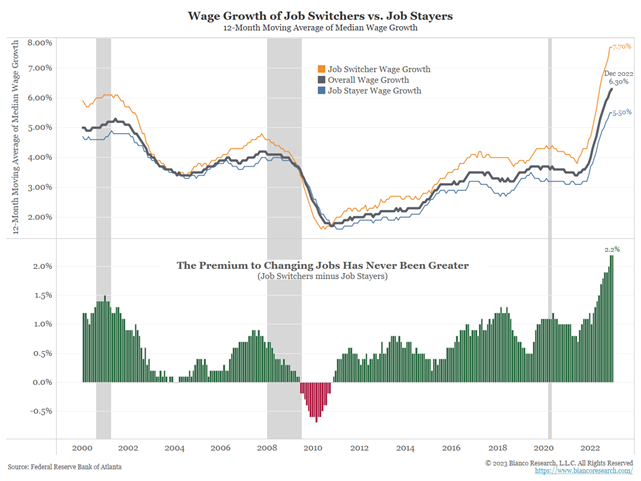

Spending behavior is significantly driven by how confident someone is in their job prospects. The chart below shows wages increasing for all workers, but if you are a “job switcher” you are rewarded even more.

Source: Federal Reserve Bank of Atlanta

The other side of the coin, for the employer, is that they must pay a competitive wage and pay more attention to their labor force, so as not to lose them to the competition.

The battle

The manifestation of this confrontation is recession, or not. The only thing we can be sure of is that this has gone on much longer than anticipated. The Fed has never raised rates this far over this short a period of time, yet they are not seeing the desired economic slowdown that will bring inflation to its knees.

Even in the face of higher prices, consumer spending behavior has not changed materially. We have seen pockets of slowing demand, but overall, the consumer marches on.

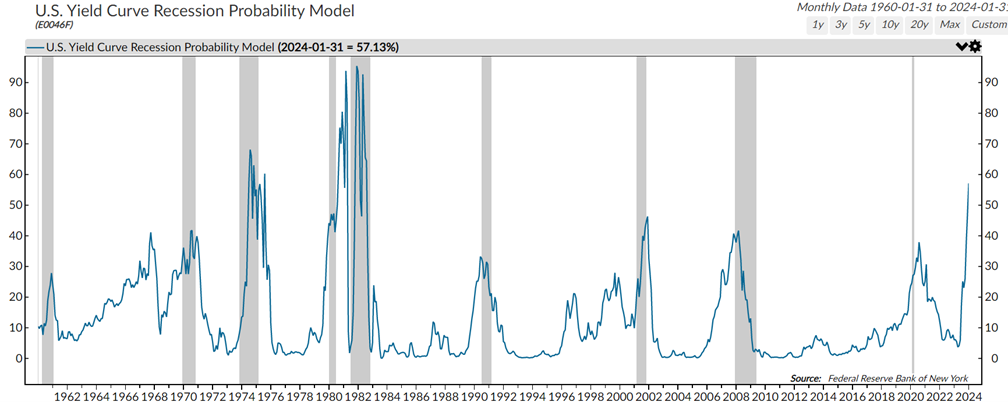

The yield curve is cited as a reliable indicator as to future economic outlook. A positive curve with short-term rates lower than longer-term indicates a strong economy as rates are stimulative to growth. The negative sloped curve portends recession, as higher short-term rates will choke off activity.

Currently, we have a negatively sloped yield curve, in both the two- to 10-year and the three-month to 10-year curves. The chart below takes these curves into account and is showing a 57% chance of recession. Last week we showed that once the curve starts to go negative, it can take an average of 311 days before we enter recession. As you can see, we are currently showing a greater probability than some earlier recessions, but not as high as some.

Source: Ned Davis Research

Wrap-up

The push-pull between the Fed and consumer will continue, even with the Fed unable to impact the demand side of the equation. Two outcomes are likely, first, the Fed will continue to raise rates, for higher and longer, pushing the economy into a recession. Second, the consumer will continue to show strength, the Fed will throw in the towel, conceding to a higher acceptable level of inflation, and there will be no recession. What is your view?!

| Upcoming Economic Releases: | Period | Expected | Previous | |

|---|---|---|---|---|

| 27-Feb | Durable Goods Orders | Jan | -4.0% | 5.6% |

| 27-Feb | Durables ex Transportation | Jan | 0.2% | -0.2% |

| 27-Feb | Capital Gds Orders Nondefense ex Air | Jan | -0.1% | -0.1% |

| 27-Feb | Pending Home Sales MoM | Jan | 1.0% | 2.5% |

| 27-Feb | Dallas Fed Manuf Activity | Feb | (9.3) | (8.4) |

| 28-Feb | Wholesale Inventories MoM | Jan | 0.1% | 0.1% |

| 28-Feb | Retail Inventories MoM | Jan | 0.2% | 0.5% |

| 28-Feb | FHFA House Price Index MoM | Dec | -0.2% | -0.1% |

| 28-Feb | MNI Chicago PMI | Feb | 45.3 | 44.3 |

| 28-Feb | Richmond Fed Manuf Index | Feb | (5) | (11) |

| 28-Feb | Conference Bd Consumer Confidence | Feb | 108.5 | 107.1 |

| 28-Feb | Conference Bd Present Situation | Feb | N/A | 150.9 |

| 28-Feb | Conference Bd Expectations | Feb | N/A | 77.8 |

| 28-Feb | Richmond Fed Business Conditions | Feb | N/A | (10) |

| 28-Feb | Dallas Fed Services Activity | Feb | N/A | (15.0) |

| 1-Mar | S&P Global US Manufacturing PMI | Feb | 47.8 | 47.8 |

| 1-Mar | Construction Spending MoM | Feb | 0.2% | -0.4% |

| 1-Mar | ISM Manufacturing | Feb | 48.0 | 47.4 |

| 1-Mar | ISM Prices Paid | Feb | 46.5 | 44.5 |

| 1-Mar | ISM Employment | Feb | N/A | 50.6 |

| 1-Mar | ISM New Orders | Feb | N/A | 42.5 |

| 1-Mar | Wards Total Vehicle Sales | Feb | 14,780,000 | 15,740,000 |

| 2-Mar | Nonfarm Productivity | Q4 | 2.5% | 3.0% |

| 2-Mar | Unit Labor Costs | Q4 | 1.6% | 1.1% |

| 2-Mar | Initial Jobless Claims | 24-Feb | 197,000 | 192,000 |

| 2-Mar | Continuing Claims | 18-Feb | 1,672,000 | 1,654,000 |

| 3-Mar | S&P Global US Services PMI | Feb | 50.5 | 50.5 |

| 3-Mar | S&P Global US Composite PMI | Feb | N/A | 50.2 |

| 3-Mar | ISM Services Index | Feb | 54.5 | 55.2 |

| 3-Mar | ISM Services Prices Paid | Feb | N/A | 67.8 |

| 3-Mar | ISM Services Employment | Feb | N/A | 50.0 |

| 3-Mar | ISM Services New Orders | Feb | N/A | 60.4 |

Mark Frears is an Investment Advisor, Executive Vice President, at Texas Capital Bank Private Wealth Advisors. He holds a Bachelor of Science from The University of Washington, and an MBA from University of Texas – Dallas.

The contents of this article are subject to the terms and conditions available here.