Fed “keeping at it” — Week of September 26, 2022

Strategy and Positioning written by Steve Orr, Chief Investment Officer; and Essential Economics written by Mark Frears, Investment Advisor

| index | wtd | ytd | 1-year | 3-year | 5-year | index level |

|---|---|---|---|---|---|---|

| S&P 500 Index | -4.36 | -21.62 | -15.73 | 9.34 | 10.01 | 3,693.23 |

| Dow Jones Industrial Average | -4.00 | -17.30 | -13.15 | 5.54 | 8.10 | 29,590.41 |

| Russell 2000 Small Cap | -6.58 | -24.50 | -24.74 | 4.33 | 4.27 | 1,679.59 |

| NASDAQ Composite | -5.06 | -30.11 | -27.23 | 11.73 | 12.13 | 10,867.93 |

| MSCI Europe, Australasia & Far East | -3.02 | -23.69 | -23.81 | -0.15 | 0.54 | 1,734.01 |

| MSCI Emerging Markets | -2.24 | -23.11 | -25.15 | -0.37 | -0.82 | 922.61 |

| Barclays U.S. Aggregate Bond Index | -1.32 | -13.54 | -14.03 | -2.90 | -0.04 | 2,036.26 |

| Merrill Lynch Intermediate Municipal | -0.92 | -8.98 | -9.09 | -0.97 | 0.85 | 291.35 |

As of market close September 23, 2022. Returns in percent.

Strategy & Positioning

— Steve Orr

Three Legs

Last week was another Bear week to forget. Bond prices fell between 1.5% and 2.5%. Stock indices fell anywhere from 3% to 5%. The tech heavy NASDAQ fell 5% and some of the very bigs — think Apple, Nvidia and Google — broke below their June lows for the first time.

To date this Bear Cycle for stocks has been fairly typical. Non-recession Bears typically last about 200 days and fall 23%. This cycle is 178 days in through last Friday and the drop from all-time highs is about 24%. This is the sixth Bear cycle that has had three separate legs of 10% or more drops. There is no consistent pattern to any of the prior cases, or guidance as to how much lower this Bear cycle will go.

Stock and bond prices fall when traders are not sure how far or how fast the Central Bank will go in shutting off the monetary spigots. We have enjoyed 12 years of easy money policies and ultra-low interest rates from Central Banks. It was an abnormal period in markets, and it took pandemic shutdowns with a gusher of monetary support to bring it to an end.

Last week the Fed continued its inflation war campaign by raising its Fed Funds target another three quarters of a percent to 3.25%. With core inflation running between 5% and 7% depending on the inflation index, the Fed has a way to go. Remember, each rate increase takes between nine and 12 months to work its way through the economy. So, the first increase back in March has yet to be fully felt throughout the economy. This is one reason why recession fears in early 2023 are rising. The concern is that the Fed will not know how much damage it is doing until it is too late. Housing is already taking the brunt of higher rates.

W-I-F-E

We have been using the initials W, I, F, E to follow the Macro pressures on our portfolios. The war news is slightly better, but we still do not have a good idea of fertilizer and crop impacts going forward. Putin is saber-rattling about nuclear options and looking for recruits. We heard one report late last week that the last open border gate with Finland had a queue over 30 kilometers long of Russians trying to leave their country.

Inflation may have already peaked, but producer and input prices staying elevated will continue to push recession risks higher, especially in Europe. Energy is key for manufacturing and home heating in the winter. Consider that Texas natural gas for delivery next month is $6.80 mm BTU. The same gas at the Netherlands hub goes for $51, a mere 7x higher. Which explains why the German government took over their largest private utility last week.

As for the Fed, Chairman Powell says he will “keep at it” (his words) until he breaks it — we hope he means inflation, not the economy. FOMC members expect the funds rate will finish this year around 4.4% and end 2023 near 4.6%. They also believe they will be successful in raising unemployment a full percent to 4.4%. That implies at least 1.5 million jobs lost. Be prepared for more layoff news. Fed Funds futures this morning are pricing rate increases for November’s meeting at three-quarters of a percent and another one-half percent at the December 14th meeting.

Remember the Fed is fighting not only Wall Street, but also Congress. The “Inflation Reduction Act” continues Congress' free-spending ways. Expect more spending to be shoved into this week’s continuing resolution to keep government open into December. Cue the “Government Shutdown” headlines in the coming days.

War, Inflation, Fed and other central banks combined are a unique mix that, to date — and we mean just right now — is causing a mild slowdown here in the US, and the beginnings of a recession in Europe and parts of Asia. There are a few signals flashing tough times ahead. OECD Composite Leading indicators down 13 of the last 14 months, are now down to 2008 -09 levels. Investor sentiment is also falling to 2008-09 levels. It usually bottoms out about five months before recessions ends but has not stopped falling yet. All the above are resetting earnings estimates lower for stocks. Once earnings estimates are lowered then prices should follow.

There will be plenty of news points over the next several weeks that will keep pressure on all markets. The first two weeks of October bring September job and then inflation reports. Mid-October starts third-quarter earnings season. Bellwether FedEx dimmed investor hopes after a dire outlook last week. Once earnings season is well underway, traders get another Fed meeting on November 2nd, and then mid-term elections.

Wrap-up

As the quarter draws to a close, one wonders about October. The Halloween month sparks fear in many investors' hearts because they remember the crashes of 1929, 1987 and big drops in 1989 and 2008. The reality is October is the 7th best month for stock returns, which is better than September’s last place. In mid-term years — October is Number One, averaging a 2.5% return. Will the War, Inflation and Fed wall of worry win out? We remain on the sidelines as our indicators grow more cautious.

Essential Economics

— Mark Frears

Keep your eye on the ball

I did not play many ball sports growing up, mainly running, and, of course, never without a frisbee in college. As I watched my boys play baseball, lacrosse and football, it was imperative that they focus on the ball. Even as I attempt to play golf, in all the things I am thinking about when standing over the ball, preparing to swing, the last one is “don’t lift up your head, watch the ball.” The Federal Open Market Committee (FOMC) is firmly in the batter’s box, with all eyes on them. What ball are they watching?

Rewind

Outside of the FOMC meeting announcement, there were some other economic releases last week. On the housing front, the National Association of Home Builders (NAHB) Index came in at 46, down from 49 in August. Building permits for August were lower than expected, but Housing Starts were above expectations and prior month.

In other releases, Jobless Claims were up slightly, showing a labor market that is still humming along. Leading Economic Index fell for the sixth consecutive month and is at its lowest level since June 2021. Eight of 10 components made negative contributions, pointing toward a slowing economy. The S&P Global US Composite Purchasing Managers' Index (PMI) showed contraction, but at a slower pace than last month.

The outlook to be gained by looking at these metrics is as clear as mud. Inflation is the focus of the market, but maybe not how you might think. While higher prices are having an impact on consumers and businesses, so far, it has not meaningfully changed behavior. The underlying economy is still making progress, albeit at a slower pace. The focus of the markets is the Fed and how high and far will they have to go to quelch inflation, with an increasing fear that the “soft landing” will not take place and a recession of some sort is in the future.

Ball

What is keeping Chair Powell and the FOMC up at night? It is the labor market. They have now raised the overnight Fed Funds rate by 2.25% in unprecedented three consecutive 75 basis point (bp) moves. While they expect some lag in impact from their rate hikes, the labor market is moving against them.

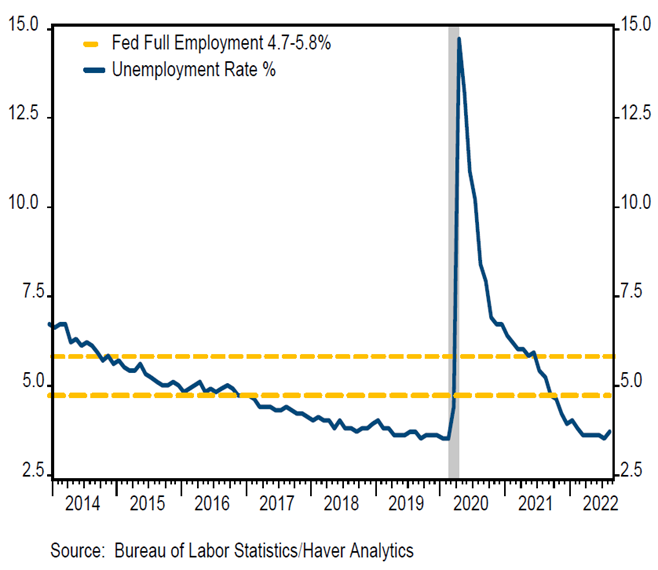

Right now, the majority of people who want to work, are working, and they are not worried about finding another job if they lose theirs as job openings are plentiful. As you can see above, the current unemployment rate is well below the FOMC’s definition of full employment, meaning more people have to be out of work for them to know they have beaten inflation by slowing the economy.

Morgan Stanley does not see job growth decelerating to its lowest growth point until mid-2023. If it takes that long, there are many more rate hikes ahead, unless a serious camp of Fed voters decides to pause and watch the lag impact.

Bottom line, if you start to see weakening in Nonfarm Payroll numbers, increased Jobless Claims, and increasing Unemployment Rate, the Fed will slow rate hikes and the bottom of the economic cycle could be in sight.

Wrap-up

While my attempts at golf are somewhat lame, the Fed is very focused. They will not take their eye off the labor ball and will continue to raise rates until they see it in their strike zone.

| Upcoming Economic Releases: | Period | Expected | Previous | |

|---|---|---|---|---|

| 26-Sep | Dallas Fed Manufacturing Activity | Sep | (10.0) | (12.9) |

| 27-Sep | Durable Goods Orders | Aug | -0.3% | -0.1% |

| 27-Sep | Durable Goods Orders ex Transport | Aug | 0.2% | 0.2% |

| 27-Sep | Cap Goods Orders Nondef ex Air | Aug | 0.2% | 0.3% |

| 27-Sep | S&P CoreLogics 20-city YoY NSA | Jul | 17.35% | 18.65% |

| 27-Sep | Conf Board Consumer Confidence | Sep | 104.5 | 103.2 |

| 27-Sep | Conf Board Present Situation | Sep | N/A | 145.4 |

| 27-Sep | Conf Board Expectations | Sep | N/A | 75.1 |

| 27-Sep | New Home Sales | Aug | 500,000 | 511,000 |

| 27-Sep | New Home Sales MoM | Aug | -2.2% | -12.6% |

| 28-Sep | Wholesale Inventories MoM | Aug | 0.5% | 0.6% |

| 28-Sep | Retail Inventories MoM | Aug | 1.0% | 1.1% |

| 28-Sep | Pending Home Sales MoM | Aug | -1.5% | -1.0% |

| 29-Sep | Initial Jobless Claims | 24-Sep | 215,000 | 213,000 |

| 29-Sep | Continuing Claims | 17-Sep | 1,383,000 | 1,379,000 |

| 29-Sep | GDP Annualized QoQ | Q2 | -0.6% | -0.6% |

| 29-Sep | Personal Consumption | Q2 | 1.5% | 1.5% |

| 29-Sep | GDP Price Index | Q2 | 8.9% | 8.9% |

| 30-Sep | Personal Income | Aug | 0.3% | 0.2% |

| 30-Sep | Personal Spending | Aug | 0.2% | 0.1% |

| 30-Sep | Real Personal Spending | Aug | 0.2% | 0.2% |

| 30-Sep | PCE Deflator YoY | Aug | 6.0% | 6.3% |

| 30-Sep | PCE Core Deflator YoY | Aug | 4.7% | 4.6% |

| 30-Sep | UM (Go MSU) Consumer Sentiment | Sep | 59.5 | 59.5 |

| 30-Sep | UM (Go MSU) Current Conditions | Sep | N/A | 58.9 |

| 30-Sep | UM (Go MSU) Expectations | Sep | N/A | 59.9 |

| 30-Sep | UM (Go MSU) 1-year inflation | Sep | N/A | 4.6% |

| 30-Sep | UM (Go MSU) 5 to 10-year inflation | Sep | 2.8% | 2.8% |

Steve Orr is the Executive Vice President and Chief Investment Officer for Texas Capital Bank Private Wealth Advisors. Steve has earned the right to use the Chartered Financial Analyst and Chartered Market Technician designations. He holds a Bachelor of Arts in Economics from The University of Texas at Austin, a Master of Business Administration in Finance from Texas State University, and a Juris Doctor in Securities from St. Mary’s University School of Law. Follow him on Twitter here.

Mark Frears is an Investment Advisor, Executive Vice President, at Texas Capital Bank Private Wealth Advisors. He holds a Bachelor of Science from The University of Washington, and an MBA from University of Texas – Dallas.

The contents of this article are subject to the terms and conditions available here.