Preparation for risk — Week of March 20, 2023

Essential Economics

— Mark Frears

Rain, rain, rain

I had the distinct pleasure of living in Seattle for a time, and the liquid sunshine was part of the package. The attraction was all the activities associated with water and mountains, plus the views! People used to be very protective of the Pacific Northwest, but eventually it was discovered. The one thing that keeps people away is the rain. It is not the thunderstorms we get in Texas, but an ongoing, slow drizzle. The benefit is the lush, green woods and foliage. Banks are currently dealing with a different form of liquidity, or lack of it.

Balance sheet

You have heard a lot about Silicon Valley Bank’s (SVB) balance sheet over the past week. What type of assets they held, the value of those assets, the liabilities to fund those assets, concentration of assets and liabilities, and their equity/capital.

The traditional bank structure used to be retail deposits funding a primarily loan-driven asset mix. Only the smaller community banks generally look like that anymore. More diverse balance sheets may be driven by opportunities arising from interest rate movements, a new client base and/or other mismatches in the financial services market. Given the balance sheet structure, you must properly manage risk through your liquidity, credit and capital lenses!

Deposits and contingent sources

One of the common themes you have heard about this week is deposit runoff. When stress in the financial system happens, banks must have enough liquidity on hand and/or proven access to it, to handle significant deposit outflows. You are more at risk if dependent on a few large deposits, as they have a significant impact on your ability to fund the bank. In addition, if a “run” on the bank’s deposits occurs, it does not take long for the media to pick up on that, and contagion can quickly spread to other areas of the bank.

Therefore, the safest funding mix is granular, small balance, sticky (relationship), and from a variety of people, business types or industries. If they are less than $250,000, then they are referred to as “insured,” as they have FDIC coverage. Most banks have a mix of insured and uninsured deposits, but you still must pay close attention to who your depositors are.

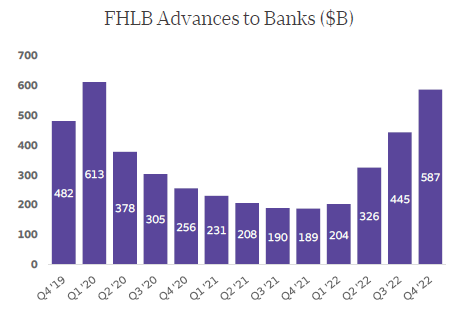

Banks hold liquidity on the balance sheet to cover any deposit outflows and have sources of contingent liquidity. The primary source of additional liquidity is borrowing from the Federal Home Loan Bank (FHLB). Most people have never heard of the FHLB system of banks. While the Fed calls itself the “lender of last resort,” the FHLB is where banks go, after they have no choice. As you can see below, banks’ need for liquidity/funding was already ramping up in Q4. Over the past week, banks borrowed over $250 million from the FHLB system.

Sources: Bloomberg, FHLB, FDIC, FRB NY, Wells Fargo Securities. FHLB advances as of Q4 2022, Fed Discount Window & BTFP as of 3/15/2023.

Some of this is for actual daily needs, but there is also a buildup of liquidity on the balance sheet when preparing for future stresses.

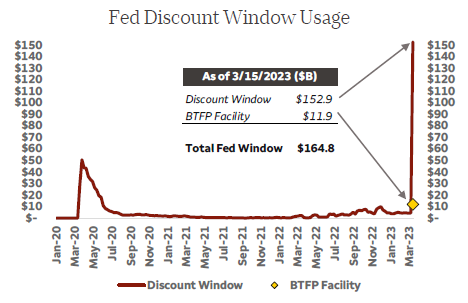

Normally, when banks borrow at the Discount Window of the Fed, there had better be a good reason, and the banks must demonstrate their plan to pay it back. Given the current environment, the Fed made the Discount Window more available, and you can see the result below.

Sources: Bloomberg, FHLB, FDIC, FRB NY, Wells Fargo Securities. FHLB advances as of Q4 2022, Fed Discount Window & BTFP as of 3/15/2023.

When banks pledge loans and securities to both of these contingent sources, they can usually only borrow as much as the assets are currently worth. This is the concept of “mark-to-market” that you have been hearing about. Securities have lost much of their underlying value as rates have risen and therefore prices for bonds bought when rates were lower are less valuable now.

In order to make plentiful liquidity available to the banking system, the Fed is allowing banks to borrow the par value of their bonds, not what they are currently worth, through the Bank Term Funding Program (BTFP). So, if a bank has a bond with par value of $100,000, which has a value in the market of $90,000, they can borrow $100,000. All the banks with bond portfolios that have lost value when rates rose (underwater is the common term), are now able to, temporarily, forget about that loss. Short-term fix.

Big picture

So, if you haven’t picked up on it yet, liquidity matters, whether we are talking about drinking water or a bank’s balance sheets.

When we run our own personal balance sheet, we have, or should have, savings set aside for emergencies or unforeseen cash flow disruptions. The amount we have on hand should align with the amount of risk we undertake. Do we have many possessions that could break, or do we work in a field that has a higher risk of layoffs? If so, you should have more savings.

The same concept applies to banks. The more risk they have on their balance sheet, the more liquidity they should have on hand. SVB had risk in their securities portfolio, with most of it having high unrealized losses. This had multiple consequences in that they could not borrow as much from it, and if they had to sell them, they would realize a loss. They had risk in their deposit base, as they were dependent on large depositors, concentrated in too few clients. They had risk in their capital/equity, as demonstrated when they were forced to sell securities because too many deposits were leaving, and they did not have enough capital to cover the losses.

Liquidity is a big deal.

Economic releases

We did have a busy week of economic releases, but due to the financial system focus, they flew below the radar. Consumer Price Index and Producer Price Index both showed lower year-over-year levels, but there is still concern about sticky inflation. We are not close to the Fed’s 2% target yet. Retail Sales declined after a significant jump in January. Housing Starts and Building permits both surprised to the upside and were largely driven by multi-family units. Consumer confidence fell in the preliminary March University of Michigan readings, although inflation expectations were lower for future periods.

Next week, the market will hear from the Federal Open Market Committee after their meeting concludes on Wednesday. Current expectations are for a 25-basis point rate hike, but we will pay more attention to the quarterly Summary of Economic Projections (SEP). We will learn their future expectations for peak Fed Funds rate, inflation though the PCE metric, and unemployment.

Given the stress placed on the financial system due to recent bank failures, the verbiage of the release and Chairman Powell’s press conference will have even greater scrutiny.

Wrap-up

While there is a cost to not having all your capital invested in your business, there can be a much larger cost if you don’t have the liquidity when you need it. Stay liquid, my friends.

| Upcoming Economic Releases: | Period | Expected | Previous | |

|---|---|---|---|---|

| 21-Mar | Philadelphia Fed Non-Manuf Activity | Mar | N/A | 3.2 |

| 21-Mar | Existing Home Sales | Feb | 4,200,000 | 4,000,000 |

| 21-Mar | Existing Home Sales MoM | Feb | 5.0% | -0.7% |

| 22-Mar | FOMC Rate Decision (Upper Bound) | 1p CDT | 5.00% | 4.75% |

| 22-Mar | FOMC Rate Decision (Lower Bound) | 1p CDT | 4.75% | 4.50% |

| 23-Mar | Initial Jobless Claims | 18-Mar | 200,000 | 192,000 |

| 23-Mar | Continuing Claims | 11-Mar | 1,690,000 | 1,684,000 |

| 23-Mar | Chicago Fed Nat Activity Index | Feb | 0.10 | 0.23 |

| 23-Mar | New Home Sales | Feb | 650,000 | 670,000 |

| 23-Mar | New Home Sales MoM | Feb | -3.0% | 7.2% |

| 23-Mar | KC Fed Manufacturing Activity | Mar | (2) | 0 |

| 24-Mar | Durable Goods Orders | Feb | 1.0% | -4.5% |

| 24-Mar | Durable Goods ex Transportation | Feb | 0.2% | 0.8% |

| 24-Mar | Cap Goods Orders Nondefense ex Air | Feb | -0.2% | 0.8% |

| 24-Mar | S&P Global US Manufacturing PMI | Mar | 47.0 | 47.3 |

| 24-Mar | S&P Global US Services PMI | Mar | 50.3 | 50.6 |

| 24-Mar | S&P Global US Composite PMI | Mar | N/A | 50.1 |

| 24-Mar | KC Fed Services Activity | Mar | N/A | 1 |

Mark Frears is an Investment Advisor, Executive Vice President, at Texas Capital Bank Private Wealth Advisors. He holds a Bachelor of Science from The University of Washington, and an MBA from University of Texas – Dallas.

The contents of this article are subject to the terms and conditions available here.